Value Added Tax (VAT) is undeniably one of the most widely implemented indirect taxes globally, currently applied by over 160 countries as a primary tool to boost government revenues, stabilize national budgets, and support long-term economic development. In the Kingdom of Saudi Arabia, the introduction and evolution of VAT represent a monumental shift in fiscal policy. Today, VAT in Saudi is recognized not merely as a tax, but as a core component of the ambitious Vision 2030 reforms. These reforms are strategically aimed at diversifying the national economy, reducing the historical dependence on oil revenues, and creating a sustainable financial future for generations to come.

Start your zatca e-invoicing journey with a system built to meet Saudi compliance. Currently levied at a standard rate of 15% on most goods and services across the supply chain, VAT has generated hundreds of billions of Riyals to fund mega-projects and public services. To enforce and monitor this massive financial ecosystem, the General Authority of Zakat, Tax and Customs (ZATCA) processes an astonishing 8.2 billion e-invoices annually through its FATOORA platform.

In this comprehensive guide, we will explore the intricate mechanism of VAT in Saudi Arabia, trace its historical development, detail the current rates and exemptions, outline the strict compliance obligations for businesses, and demonstrate how utilizing an advanced platform like Daysum can streamline your tax reporting and protect your enterprise from costly penalties.

Definition and Core Concept of Value Added Tax (VAT)

To navigate the regulatory landscape in Saudi Arabia, one must first deeply understand how VAT functions on a foundational level. Value Added Tax is defined as an indirect tax levied on all goods and services as they pass through multiple stages of the supply chain—from initial raw material production, to manufacturing, to wholesale distribution, and finally to the point of retail sale.

The Mechanism of Input and Output VAT

Unlike a traditional sales tax that is only collected once at the final point of purchase, VAT is fractional.

- Output VAT: This is the tax a business charges and collects from its customers when it sells a product or service.

- Input VAT: This is the tax a business pays to its suppliers when purchasing raw materials, inventory, or operational services.

Businesses act as the government’s official intermediaries in this process. At the end of every tax period (monthly or quarterly), a company calculates the total Output VAT it collected and subtracts the total Input VAT it paid. The business then remits the “net difference” to ZATCA. If the Input VAT exceeds the Output VAT, the business is entitled to reclaim the difference as a tax refund.

Ultimately, the final consumer—the everyday shopper—bears the total burden of the tax, as they cannot reclaim the VAT paid on personal purchases. By utilizing a robust electronic invoice ksa solution, companies can automate this complex tracking process, ensuring that every halala of Input and Output VAT is meticulously recorded and reported.

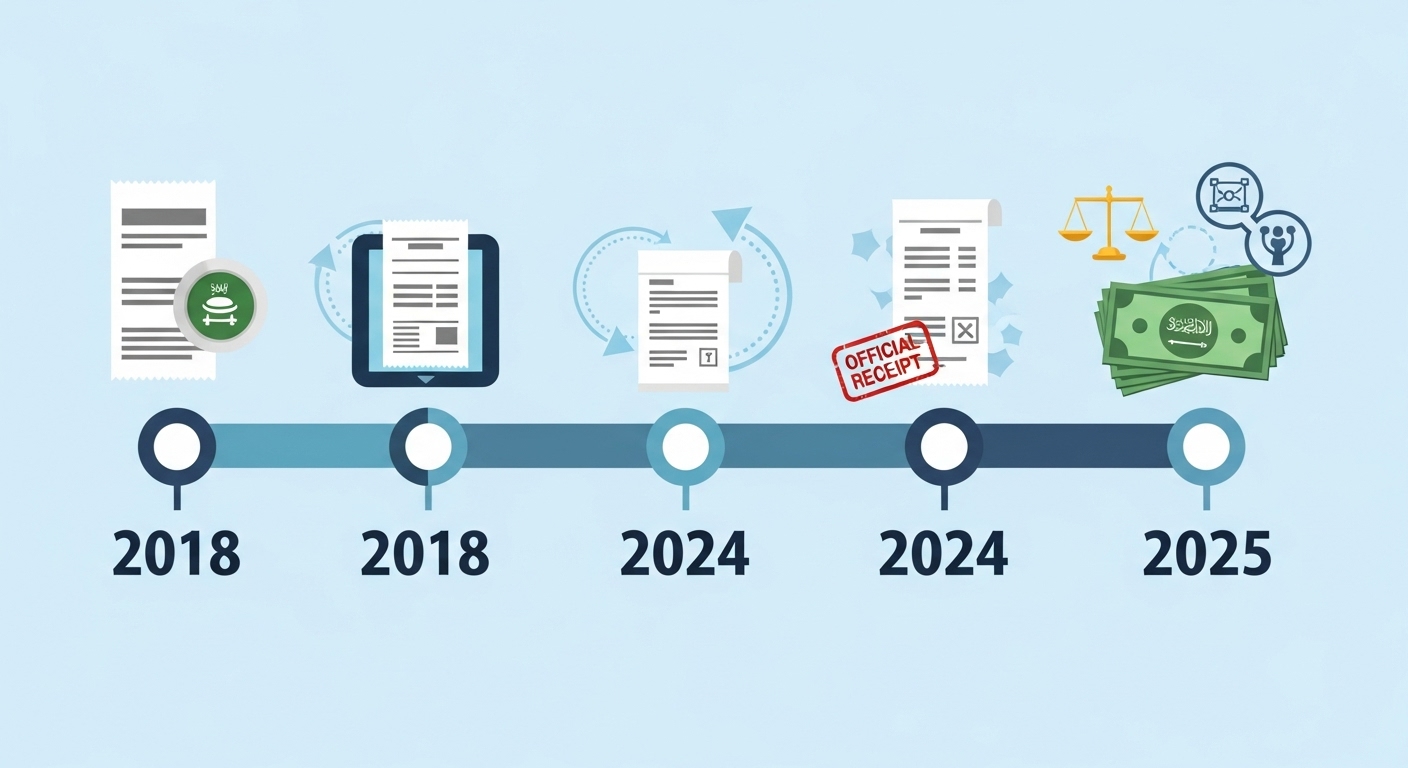

The Historical Timeline and Evolution of VAT in KSA

The implementation of VAT in Saudi Arabia did not happen overnight. It was the result of careful regional planning, economic forecasting, and responsive policy adjustments to global market conditions. Understanding this timeline is crucial to appreciating the current tax landscape.

June 2016: The GCC Unified Agreement

The conceptual groundwork was laid in June 2016 when the Gulf Cooperation Council (GCC) countries formally approved the implementation of a unified VAT framework. The goal was to establish a cohesive economic bloc, prevent tax evasion across borders, and create a standardized revenue stream for the Gulf states amid fluctuating global oil prices.

February 2017: Saudi Arabia Ratifies the Agreement

Saudi Arabia officially ratified the GCC agreement in early 2017. The Ministry of Finance and ZATCA immediately began a nationwide awareness campaign to prepare businesses, accountants, and consumers for the upcoming economic shift, initially setting the standard tax rate at a highly competitive 5%.

January 2018: The Official 5% Launch

On January 1, 2018, via Royal Decree M/113, VAT was officially introduced into the Saudi economy at a rate of 5%. This smooth rollout marked a historic milestone for the Kingdom, successfully integrating millions of transactions into a newly established digital tax registry.

July 2020: The Strategic Increase to 15%

In May 2020, as the global economy faced unprecedented challenges due to the COVID-19 pandemic and plummeting oil prices, the Saudi government took decisive action to protect its economy. Royal Decree No. (A/638) was issued to increase the VAT rate from 5% to 15%. This bold adjustment, which took effect on July 1, 2020, was a necessary economic stabilizer. It ensured that the government could continue funding vital healthcare services, infrastructure development, and Vision 2030 mega-projects without compromising the nation’s financial reserves.

Strategic Objectives of the VAT System

The imposition of a 15% VAT serves multiple strategic, long-term objectives that align perfectly with the Kingdom’s broader economic blueprint:

- Enhancing Non-Oil Government Revenues: VAT has proven to be an incredibly reliable revenue stream. It is estimated to generate over SAR 200 billion annually. These funds are directly injected into national infrastructure, public transportation, healthcare facilities, and educational institutions.

- Funding Vision 2030 Mega-Projects: The continuous flow of VAT revenue supports the capital required for transformative projects such as NEOM, the Red Sea Project, and Qiddiya, which are set to revolutionize the Kingdom’s tourism and technology sectors.

- Achieving Consumption-Based Equity: By shifting the tax burden to consumption rather than personal income, the system ensures a high degree of fairness. Individuals who consume luxury goods and spend more bear a proportionally higher share of the tax, while the government continues to provide essential subsidies and welfare programs for lower-income citizens.

The Step-by-Step Mechanism of Tax Implementation

For the VAT system to function flawlessly across millions of daily transactions, each stakeholder in the economy has specific, highly regulated roles.

The Role of Businesses and Enterprises

Businesses are the vital cogs in the VAT machine. They are legally mandated to:

- Charge and Collect: Accurately apply the 15% (or 0%) VAT rate to all taxable supplies at every stage of the sale.

- Issue Compliant Invoices: Generate real-time, highly structured XML invoices featuring cryptographic stamps and QR codes that comply fully with ZATCA’s FATOORA Phase 1 and Phase 2 mandates.

- File Periodic Returns: Consolidate their financial data and submit accurate tax returns to ZATCA either monthly (for large enterprises exceeding SAR 40 million in revenue) or quarterly (for smaller businesses).

The Role of the Consumer

Consumers participate passively but essentially. Whenever they purchase a coffee, buy a car, or pay for a consulting service, the 15% VAT is already embedded in the final price displayed to them. They pay the total amount, trusting that the merchant will remit the tax portion to the government.

The Role of ZATCA and the Government

The government, represented by ZATCA, operates the digital infrastructure. ZATCA receives the net difference between the VAT collected from sales and the VAT paid on business purchases. Through the FATOORA system, ZATCA monitors these transactions in real-time, utilizing advanced data analytics to flag discrepancies, audit suspicious returns, and process legitimate tax refund requests rapidly.

VAT Rates, Scope, and Exemptions in Saudi Arabia

To ensure economic balance and protect certain vital sectors, the Saudi VAT system classifies goods and services into three distinct categories. Understanding these classifications is critical for accurate accounting and pricing.

|

VAT Rate Classification |

Scope of Application and Examples |

Economic Rationale |

|

Standard Rate (15%) |

Applied to the vast majority of commercial goods and services. This includes electronics, vehicles, clothing, telecommunication services, professional consulting, dining at restaurants, and domestic transportation. |

Serves as the primary engine for generating government revenue and funding public services. |

|

Zero-Rated (0%) |

Applied to specific strategic sectors. Businesses charge 0% on sales but can still reclaim the Input VAT paid on their expenses. Includes: Exports outside the GCC, international transport (land, air, sea), qualifying medicines and medical goods, and certain eligible industrial investments. |

Designed to boost the global competitiveness of Saudi exports and support the international logistics and healthcare sectors. |

|

Fully Exempt |

No VAT is charged on the sale, and the business cannot reclaim Input VAT on related expenses. Includes: Residential real estate rentals, specific financial services (like life insurance or margin-based loans), and certain health/education services provided by licensed public entities. |

Intended to reduce the cost of living for residents by keeping essential housing and basic financial services untaxed. |

VAT Registration Thresholds and Guidelines

Not every business in Saudi Arabia is required to register for VAT. ZATCA has established clear revenue thresholds to alleviate the administrative burden on micro-businesses while capturing revenue from established enterprises.

- Mandatory Registration: Any business whose taxable annual revenues exceed SAR 375,000 must register for VAT within 30 days of reaching this threshold. Failure to do so results in severe financial penalties.

- Voluntary Registration: Businesses with annual revenues between SAR 187,500 and SAR 375,000 have the option to register voluntarily. Many startups choose this route because it allows them to reclaim the Input VAT they pay on expensive initial setup costs, equipment, and marketing.

- Exemption from Registration: Businesses whose entire revenue is generated from fully VAT-exempt activities (such as a landlord who only leases residential apartments) are not required to register for VAT, regardless of their total income.

Strict Business Obligations and E-Invoicing Mandates

Registering for VAT is only the beginning. Once registered, a business must adhere to a strict set of operational and administrative obligations to remain in good standing with the government.

- Records Retention: The law mandates that businesses must maintain all financial records, tax invoices, accounting ledgers, and customs documents for a minimum of 6 years. In cases involving real estate, this period extends to 15 years.

- Clear VAT Display: Businesses must ensure that all prices displayed to retail consumers include VAT. On the official tax invoice, the total price excluding VAT, the exact VAT amount, and the total inclusive price must be displayed on separate, clearly visible lines.

- ZATCA-Approved E-Invoicing: Perhaps the most rigorous obligation is the implementation of electronic invoicing. Businesses can no longer use handwritten receipts or basic word processors. They must utilize ZATCA-approved e-invoicing software that securely generates, hashes, and archives invoices while communicating with the national FATOORA platform.

For large-scale operations looking to streamline these complex obligations across multiple departments, undertaking a full odoo implementation saudi arabia through a certified partner ensures that VAT compliance is natively baked into inventory, sales, and purchasing workflows.

Penalties, Fines, and Enforcement for Non-Compliance

ZATCA wields considerable authority to enforce compliance and heavily penalize negligence or intentional tax evasion. The financial penalties are designed to be a strong deterrent:

- Late Registration: Failing to register for VAT when mandatory results in a fine of SAR 10,000.

- Late Filing or Payment: Failing to file a tax return on time incurs a penalty ranging from 5% to 25% of the tax due. Furthermore, late payment of the actual tax amount attracts an additional fine of 5% for every month the payment is delayed.

- Non-Compliant Invoicing: Issuing a paper invoice or an electronic invoice that lacks the mandatory QR code or XML structure can result in compounding fines starting at SAR 1,000 and escalating rapidly for repeat offenses.

- Tax Evasion: The most severe penalties are reserved for intentional tax evasion, data manipulation, or submitting fraudulent refund claims. These crimes can result in fines up to 50% of the evaded tax amount, suspension of commercial licenses, and potential criminal prosecution.

Compliance Tools: A Competitor Cloud Pricing Comparison

To avoid these devastating fines, Saudi businesses must invest in reliable accounting and ERP software. The market offers various solutions, but they differ significantly in capability, cost, and depth of ZATCA integration. Below is an objective comparison of the top software providers available to Saudi enterprises:

|

Software Provider |

Core VAT & ZATCA Features |

Estimated Annual Cost (SAR) |

Market Focus |

|

Daysum |

Fully automated net VAT calculation, instant XML reporting, Phase 2 compliance, and deep ERP integration. |

SAR 750 |

The absolute best value for Saudi SMEs needing comprehensive compliance and management. |

|

Wafeq |

Easy generation of quarterly returns, good handling of exemptions, and regional multi-currency support. |

SAR 1,200 |

Targeted at service-based small businesses and freelancers. |

|

SMACC |

Strong VAT registration tools, reliable POS integration, and input tax recovery tracking. |

SAR 1,500 |

Geared towards traditional retail chains upgrading to the cloud. |

|

Qoyod |

Automated auto-filing features, advanced financial dashboards, and detailed ledger management. |

SAR 2,000+ |

Suitable for medium to large enterprises with higher software budgets. |

As the comparison highlights, while there are many capable systems on the market, they often come with steep price tags. Daysum stands out by offering enterprise-grade VAT compliance and ERP functionalities at a fraction of the cost, making it the most optimized choice for a growing Saudi enterprise.

Why Daysum is the Ultimate Partner for Saudi SMEs

Navigating the complexities of the 15% standard rate, zero-rated exports, and fully exempt services is a daunting task for any business owner. You need software that does the heavy lifting for you.

Daysum is engineered specifically to align with Saudi Arabia’s unique economic landscape and ZATCA’s stringent Phase 2 e-invoicing requirements. When you choose Daysum, you are investing in a system that:

- Automates the Math: Daysum instantly calculates Output VAT on sales and tracks Input VAT on expenses, generating a flawless net-tax report at the end of your billing cycle.

- Industry-Specific Mastery: If you operate in complex sectors with volatile pricing and specific tax treatments, standard software will fail. Daysum offers tailored modules, acting as the best gold accounting software for jewelers by separating raw material costs from taxable making charges effortlessly.

- Unifies Your Business: Beyond just taxes, Daysum integrates your entire workforce. By deploying their cloud hrms solutions, you can manage payroll, employee expenses, and VAT-deductible corporate purchases from a single, centralized, highly secure dashboard.

By adopting Daysum, you transition from worrying about tax compliance to focusing entirely on business growth, knowing that your financial operations are legally sound, highly efficient, and perfectly aligned with the future of Saudi commerce.

Conclusion

The introduction and evolution of VAT in Saudi Arabia serves as a successful, globally recognized model of smart economic reform. By meticulously balancing the enhancement of non-oil government revenues with the protection of vital societal sectors through carefully designed zero-rates and exemptions, the Kingdom has fortified its fiscal future.

For businesses, VAT is no longer a looming challenge; it is an integrated reality of daily operations. With ZATCA processing over 8.2 billion e-invoices annually, the margin for manual error has vanished. By understanding the historical context, the operational mechanisms, and the strict compliance obligations, businesses can navigate this landscape successfully. Utilizing powerful, cost-effective tools like Daysum ensures that your enterprise not only adheres to the Kingdom’s rigorous standards of transparency and efficiency but also establishes itself as a highly competitive player in the thriving Saudi economy.

Frequently Asked Questions (FAQs)

Yes, under specific conditions outlined by ZATCA, a business can reclaim Input VAT incurred prior to its official registration date. Generally, you can claim VAT paid on capital assets (like machinery or heavy equipment) purchased up to 5 years before registration, and on standard goods or services purchased up to 6 months before registration. However, these goods must still be in the possession of the business and used for taxable activities, and you must possess the original, compliant tax invoices to prove the purchase.

While both result in the customer paying 0% tax on the transaction, the accounting impact on the business is completely different. If you sell a "Zero-Rated" good (such as exporting a product to Europe), your sale is still considered part of the taxable VAT system; therefore, you are legally allowed to reclaim the Input VAT you paid on the materials used to make that product. Conversely, if you provide an "Exempt" service (like residential leasing), you are outside the VAT chain for that specific activity, meaning you absolutely cannot reclaim the Input VAT you paid on expenses related to that service (like maintenance or building repairs).

No, absolutely not. Under ZATCA's strict e-invoicing regulations, once a tax invoice is generated, cryptographically stamped, and issued, it cannot be deleted, altered, or overwritten under any circumstances. If an error was made regarding the price or the VAT amount, the only legally compliant way to correct it is to issue an electronic "Credit Note" (to reduce the amount owed) or a "Debit Note" (to increase the amount owed). This note must explicitly reference the original invoice's unique UUID to ensure a transparent, auditable paper trail.

Yes. Because Daysum is a true Cloud-Based ERP system, you do not have to worry about manual updates, downloading patches, or hiring IT professionals to modify your software. When ZATCA introduces new compliance mandates, reporting protocols, or technical API shifts for the FATOORA platform, the Daysum engineering team updates the central cloud infrastructure. These updates are deployed automatically in the background, ensuring that your business remains 100% compliant and fully operational without any disruptive downtime.